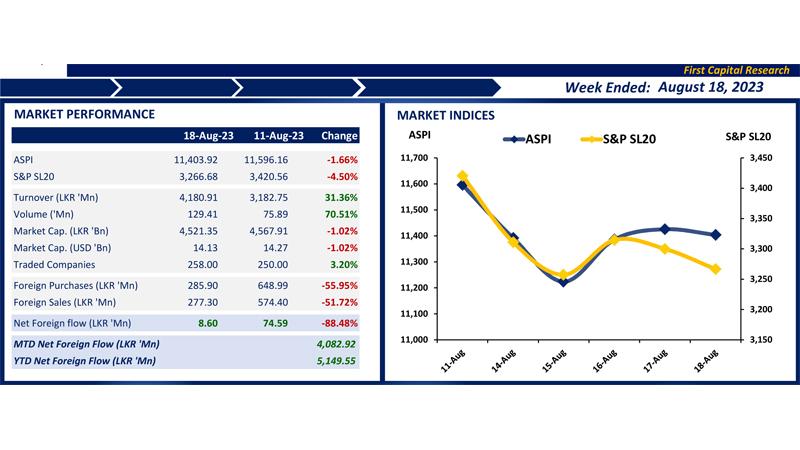

The Sri Lankan stock market experienced a week of mixed activities and volatile trading sessions, fluctuating between gains and losses. The week concluded with the index closing at 11,404, reflecting a decline of 192 points.

In the beginning, profit booking extended with significant foreign selling mainly on the Blue chip and Banking counters (COMB, SAMP and HNB) which significantly dragged the index to red. As the week progressed, ASPI was largely supported by the NBFIsmainly CFIN and PLC after the GoSL lifted the import ban on heavy vehicles (buses, trucks and tankers) for the first time since March 2020

While the initial days of the week witnessed some selling pressure in the treasury sector, a bullish trend emerged around mid-week. This upswing was driven by the release of quarterly results of CFVF, CALT and FCT, which revealed earnings surpassing expectations at over LKR 2.5Bn. These positive results were attributed to a significant reduction in interest rates, coupled with an economic rebound.

Despite backing the ASPI, the Banking, Diversified Financials, and Capital Goods sectors remained prominent contributors to the overall market turnover. Notably, the average market turnover exhibited a 33.8% improvement compared to the previous week, to LKR 3.9Bn.

This improvement was buoyed by active retail participation while off-board transactions involving High Net Worth investors further bolstered market turnover.

Foreign investors turned net sellers with high participation and recording a net foreign outflow of Rs 659.0 mn. Meanwhile, MELS remained the top foreign inflow while JKH, SAMP and HNB were the three counters recording the largest foreign outflow during the week.

As anticipated, the conclusion of the quarterly results reporting period shed light on the performance of various sectors.

The Banking sector notably exhibited the most substantial YoY growth in terms of earnings, followed by the Telecommunication sector. In a positive development, the tourism industry demonstrated a faster-than-expected revival, with tourist arrivals exceeding 800,000YTD. Consequently, several hotels reported profitable quarters, with some managing to mitigate losses on a YoY basis.

Conversely, the Food, Beverage, and Tobacco sector faced YoY earnings contraction, attributed to reduced prices and a slow recovery in volumes. However, there was a marginal improvement in earnings on a QoQ basis.

This improvement was partly due to the alleviation of finance costs, stemming from a decline in the AWPLR, which had previously exerted considerable pressure on earnings.

Courtesy: First Capital Research