First Capital Research (FCR) in its Mid Year outlook for 2024 states that the past 12 months has been a recovery phase for Sri Lanka.

First Capital Research (FCR) in its Mid Year outlook for 2024 states that the past 12 months has been a recovery phase for Sri Lanka.

The country re-emerged with positive growth, while most macroeconomic indicators recovered with inflation falling and remaining below 3%.

Sri Lanka has managed to fulfill most conditions of the IMF program with completion of Domestic Debt Restructuring and reaching a deal for external debt restructuring being the big win.

“However, progress on state Owned Enterprise (SOE) reforms and targeted privatisations has been slow.”

The report states that External Debt Restructuring (EDR) is the key requirement for Sri Lanka, in the current context which supports Sri Lanka to achieve debt sustainability and providing the most important credit rating upgrade removing the country from its default status (RD).

The country now moves into a 12-month period of elections which may delay or stall the EDR process.

“Despite elections, IMF program continuity would be vital for the country as continuous reforms ensures stability and sustainability. “The country or the new leadership may not have too much time to get on with the reforms, if not the country may move further deep into the crisis,” the report adds.

Last year, Sri Lanka posted a primary surplus of Rs. 173Bn after 5 years and for the 6th time since 1950, driven by higher tax collections and reduced capital expenditure. “Continuing under the IMF program, we expect the primary surplus to continue in 2024E (0.8% of GDP) as well while the budget deficit is expected to reduce to 7.1% of GDP.”

The report also said that Foreign reserves surpassed Rs. 5.6 Bn in July 2024, highest in 43 months after December 2020.

“USD/Rs. is expected to remain stable 2H2024 while economic recovery and consumer demand may influence some depreciation towards 1H2025 allowing the currency to trade within a range of Rs. 305.0- 315.0 over the next 12 months (Jun-25)”

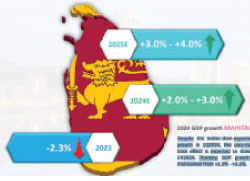

“Despite the better-than-expected recovery and growth in 1Q2024, the uncertainty and higher base effect is expected to slowdown growth in 2H2024. Thereby, GDP growth expectation is maintained from +2.0% – +3.0%.”

FCR outlook commenting on Inflation says that for remainder 2024 end it remains unchanged, with annual average inflation expected to remain around the 4.0%-7.0% range.

“However, FCR expects inflation to gradually pickup in 2025 end but to remain below the 5.0% target level.”

CCPI declined steeply and continued to remain well below 5.0% in 1H2024 with Jul-24 recording 2.4%.