Sri Lanka’s economic crisis fuelled by unsustainable debt and a default in 2022, left the country struggling to stabilise its economy. Its high climate vulnerability that disrupts livelihoods exacerbated the economic challenges. In the face of dual pressure from an economic crisis and climate vulnerability, the need for alternative approaches to financial recovery has never been more urgent. Therefore, debt-for-climate-and-nature (DfCN) swapscould be a possible option to lower the financial burden while addressing climate challenges.

Need for alternative financing options

Sri Lanka was forced to default on its external debt and seek a USD 3 billion bailout from the International Monetary Fund (IMF)in March 2023. Its total debt stock stood at USD 92 billion, with 40% being external debt in 2023. Sri Lanka’s debt portfolio is complex and its outstanding debt to China and India accounted for 18% of total external debt (59% of bilateral loans) in September 2022 (Figure 1). Amidst the conclusion of debt restructuring, Sri Lanka might benefit by opening to alternative financial instruments.

DfCN swaps as an alternative

DfCN swaps are a sovereign debt restructuring tool that helps (partial) restructuring of external debt in exchange for domestic investment in climate action. Well-designed DfCN swaps provide debtor countries the fiscal space to invest in climate adaptation and biodiversity sustainability.

DfCN swaps are a sovereign debt restructuring tool that helps (partial) restructuring of external debt in exchange for domestic investment in climate action. Well-designed DfCN swaps provide debtor countries the fiscal space to invest in climate adaptation and biodiversity sustainability.

With unsustainable debt and climate change identified as pressing issues for developing countries, Sri Lanka emerges as a priority country for DfCN swaps. Earlier, DfCN swaps followed a ‘piecemeal approach’– implementing smaller, uncoordinated projects and managing funds through extrabudgetary channels.

In contrast, recent swaps follow a ‘systematic approach’ – focusing on broader programes instead of individual projects and providing budget support by channelling funds directly into debtor countries’ national budgets.This approach makes DfCN swaps more effective by mobilising larger amounts of funds, increasing debtor governments’ accountability, linking payments to performance, and aligning Nationally Determined Contributions (NDCs) and National Biodiversity Strategies and Action Plans (NBSAPs) in target setting.

Global context, debt swap options

DfCN swaps was first introduced in 1984 in response to the deteriorating tropical rain forests and mounting debt obligations in Latin America. Since then, many countries have adopted DfCN swaps to address both financial and environmental challenges.

In 2002, the United States (US) engaged in a bilateral swap with Peru, subsidised by NGOs such as The Nature Conservancy (TNC), to protect over 1 million hectares of wilderness areas. The US has also engaged in similar swaps with Guatemala and Indonesia to protect tropical forests.

In 2015, Seychelles, pioneered a Blue Economy debt for nature swaps, converting USD 21.6 million of sovereign debt with Paris Club creditors to fund marine conservation. This is considered the world’s first debt swap for ocean conservation and climate adaptation.

Belize engaged in a ‘tripartite blue economy swap’ with the TNC in 2021, which reduced its external debt by 10% of GDP. TNC helped Belize to buy back USD 553 million of national debt borrowed from commercial creditors (30% of GDP) by issuing USD 346 million in blue bonds (10% of GDP). In response, Belize agreed to invest in marine conservation. This deal allows buy back of entire external commercial debt by TNC and Belize to invest USD 4 million annually on marine conservation until 2041aiming to increase marine-protection parks from 15.9% of its oceans to 30% in 2040. Hence, this deal addresses the triple objectives of restoring debt sustainability, promoting sustainable development and enhancing climate resilience.

World’s largest DfCN swap

In 2023,Ecuadorentered into the world’s largest DfCN swap, facilitated by Credit Suisse, buying back USD 1.6 billion of sovereign debt for USD 656 million in new sovereign debt. In return, Ecuador agreed to allocate USD 450 million in long-term marine conservation in the Galápagos Islands.

The success of this deal was driven by several key factors: participation of academia, collaboration and consensus among multiple stakeholders including civil society and local governments, an innovative financing model, and government leadership.

The effectiveness of swaps depends onthe ability to address several key challenges: political and macroeconomic stability to ensure long-term accomplishment; stable institutional structures to denote stability in planning and implementation; strong regulatory frameworks to cover both financial and environmental obligations; and knowledge/skills on swaps at every level of the public service.Accordingly, the success of DfCN swaps is dependent on the leadership role of debtor governments and a systematic approach in the designing and implementation of swaps.

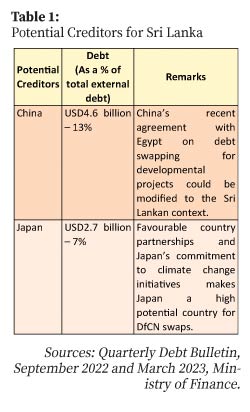

Debt swaps are determined collectively by the respective parties involved, hence, it is difficult to predict the magnitudes of these swaps. However, following the three criteria proposed by Boland (2023) on the magnitude of debt, type of lending (whether it is a commercial or concessional loans) and interest of the creditors (considering the country’s track record), Sri Lanka may consider the following four creditors for a possible DfCN swap in the future (Table 1).

Way forward

In addressing the triple challenges of high indebtedness, climate change and loss of nature, DfCN swaps can serve as an effective alternative fiscal instrument for debt-ridden Sri Lanka. Systematic planning and stringent government commitment and all relevant key stakeholders are crucial for its success. Also, addressing knowledge and skill gaps on debt swaps is crucial. With sufficient political and macro-stability, Sri Lanka could be ready to implement DfCN swaps potentially accelerating its economic recovery.

Lakmini Fernando is a Research Fellow at IPS with primary research interest in Development Economics, Public Finance and Climate Change.

Sunimalee Madurawala is a Research Economist at the Institute of Policy Studies of Sri Lanka (IPS).